Please refer to page 5, which shows the factors behind year-on-year changes.

By segment, in the Processed Foods Business, internal factors contributed an increase of JPY 4.4 billion, while external factors resulted in a decrease of JPY 4.6 billion, leading to a slight decline in profit compared with the previous year.

In the Meat Products Business, ordinary profit increased by JPY 10.3 billion year on year, driven by an increase of JPY 4.8 billion from domestic business factors and JPY 5.2 billion from overseas factors.

Further details will be explained later by the heads of each business division.

Please refer to the right-hand side of page 23, which shows revenue by region.

Breaking down the JPY 82.6 billion increase in revenue between Japan and overseas, revenue in Japan increased by JPY 18.9 billion. This was driven by the Processed Foods Business, where we implemented a campaign linked to a popular animated movie for ham and sausage products, strengthened our brands, and carried out price revisions. In the Meat Products Business, the increase was mainly due to higher selling prices, particularly for domestically produced chicken.

Overseas, revenue increased by JPY 63.8 billion, supported by strong sales growth primarily in North America, as well as the impact of the change in ANZCO’s fiscal year-end.

As a result, the overseas revenue ratio rose by 4.8 percentage points year on year to 19.8%.

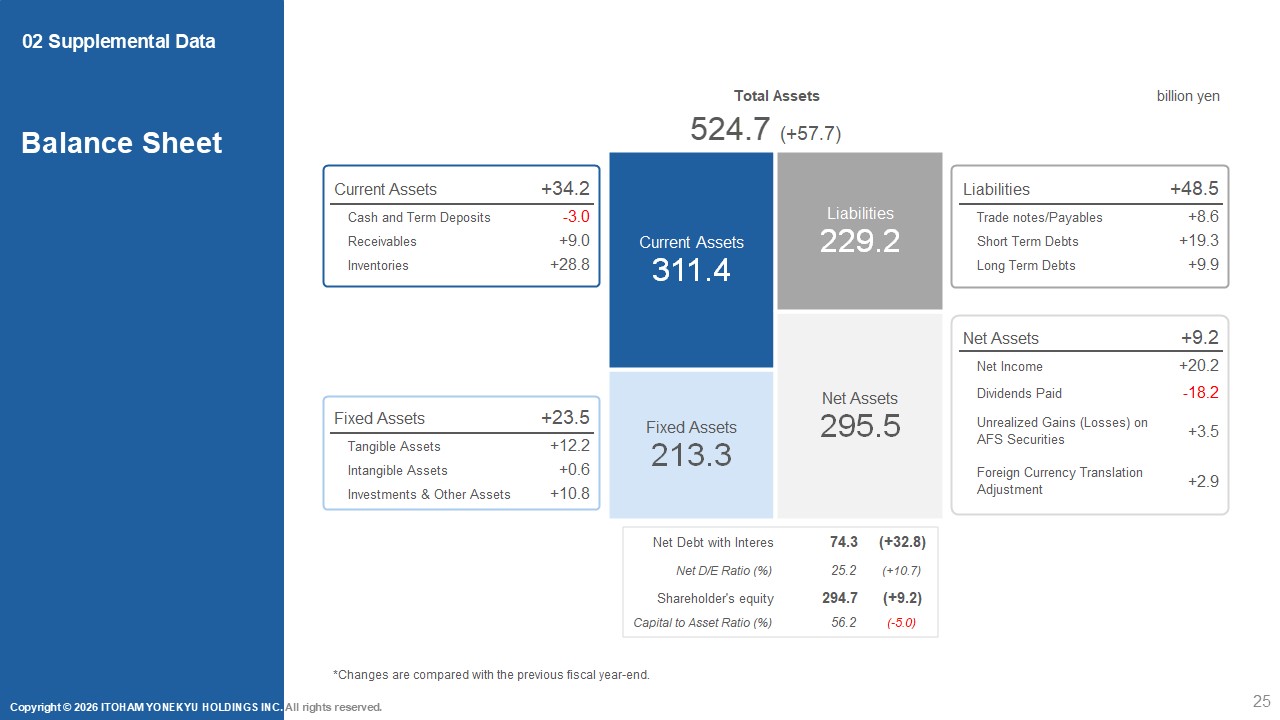

Please refer to page 25, which shows the balance sheet. Total assets increased by JPY 57.7 billion year on year to JPY 524.7 billion. Looking at assets, notes and accounts receivable increased by JPY 9.0 billion, mainly due to higher selling prices. Inventories increased by JPY 28.8 billion overall, driven primarily by an increase of JPY 16.6 billion at ANZCO in the Meat Products Business, as well as a JPY 14.1 billion increase in domestically held imported meat inventories, reflecting higher unit prices and larger inventory volumes.

On the liabilities side, notes and accounts payable increased by JPY 8.6 billion, and short-term borrowings rose by JPY 19.3 billion, mainly due to an increase in working capital in Japan. In addition, we raised funds for the construction of the new Mishima plant, resulting in a JPY 9.9 billion increase in long-term borrowings. With respect to shareholders’ equity, retained earnings increased by JPY 20.2 billion from net profit, while dividends paid totaled JPY 18.2 billion.

Within other comprehensive income, the valuation difference on available-for-sale securities increased by JPY 3.5 billion, and the foreign currency translation adjustment increased by JPY 2.9 billion.

As a result of these factors and other changes, net assets increased by JPY 9.2 billion to JPY 295.5 billion.

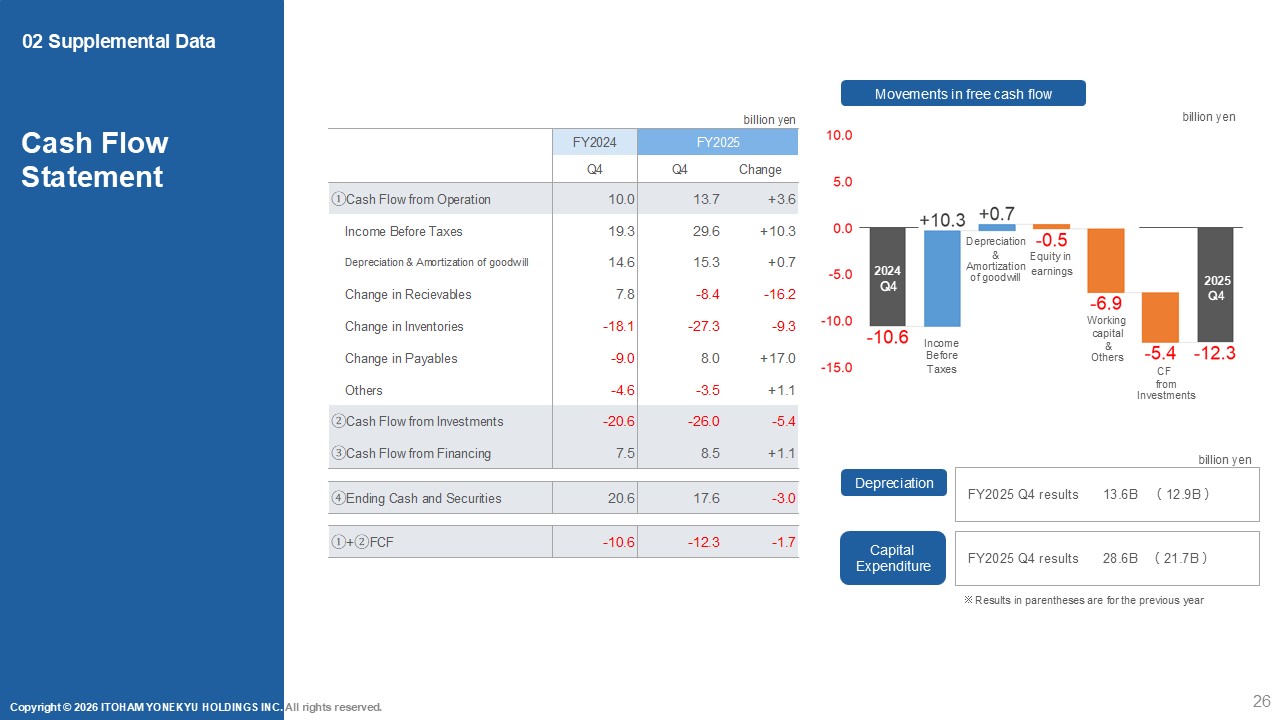

Please refer to page 26, which shows the statement of cash flows.

Cash flows from operating activities resulted in a cash inflow of JPY 13.7 billion. Although profits accumulated during the period, the increase in inventories limited the improvement to JPY 3.6 billion compared with the previous year.

Cash flows from investing activities resulted in a cash outflow of JPY 26.0 billion, mainly due to the acquisition of property, plant and equipment.

As a result of the construction of the new Mishima plant, cash outflows increased by JPY 5.4 billion year on year. As a result, free cash flow, which is the sum of cash flows from operating and investing activities, decreased by JPY 1.7 billion year on year to negative JPY 12.3 billion.

Cash flows from financing activities resulted in a cash inflow of JPY 8.5 billion. While short-term borrowings increased by JPY 18.2 billion and long-term borrowings increased by JPY 10.0 billion, this was partly offset by dividends paid of JPY 18.1 billion and repayments of lease liabilities of JPY 1.4 billion. Compared with the previous year, cash inflows increased by JPY 1.1 billion.

Cash and cash equivalents at the end of the period amounted to JPY 17.6 billion. Due to efforts such as reducing on-hand cash, this represents a decrease of JPY 3.0 billion year on year.

Capital expenditures amounted to JPY 28.6 billion, primarily reflecting JPY 9.1 billion in construction in progress related to the Mishima plant, as well as renewal of domestic facilities, reconstruction of core IT systems, and investments overseas to improve production efficiency at ANZCO.

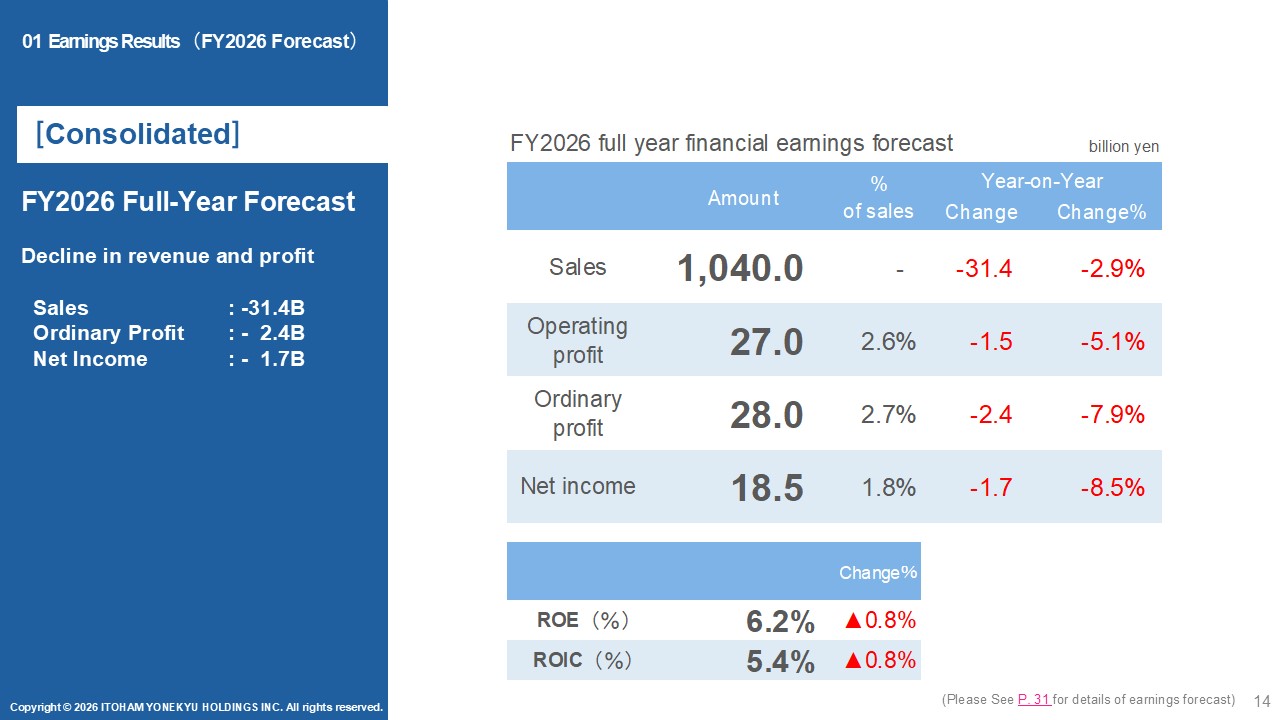

Returning to the materials, please refer to page 14, which shows the full-year performance forecast for fiscal year 2026. We forecast revenue of JPY 1,040.0 billion, operating profit of JPY 27.0 billion, ordinary profit of JPY 28.0 billion, and profit attributable to owners of the parent of JPY 18.5 billion.

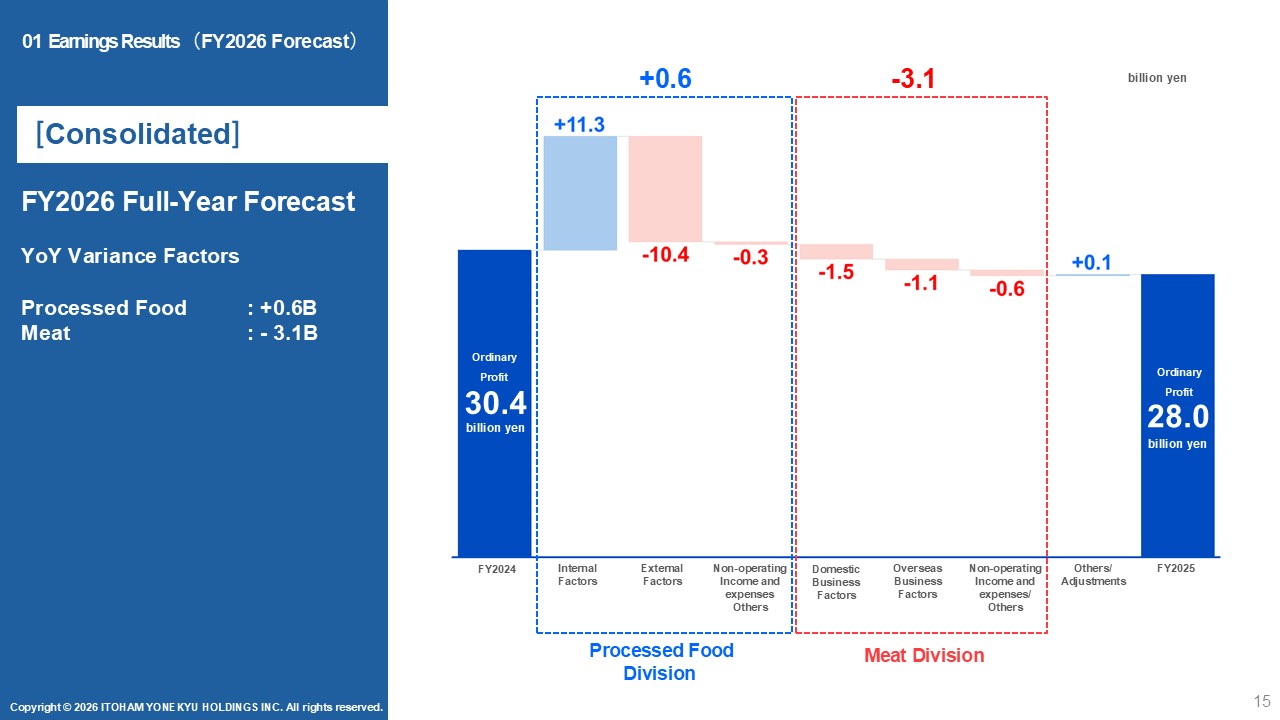

Please refer to page 15, which outlines the factors behind the year-on-year changes in the full-year forecast for fiscal year 2026. In the Processed Foods Business, raw material costs are expected to increase; however, internal factors are expected to contribute a profit increase of JPY 0.6 billion.

In contrast, the Meat Products Business is expected to see a decrease of JPY 3.1 billion, reflecting a reactionary decline in market conditions in the domestic business and the impact of the fiscal year-end change and other factors in overseas operations.

That concludes my explanation.

Ito:

Next, this is Ito, I will explain the full-year results for fiscal year 2025 and the full-year forecast for fiscal year 2026 for the Processed Foods Business.

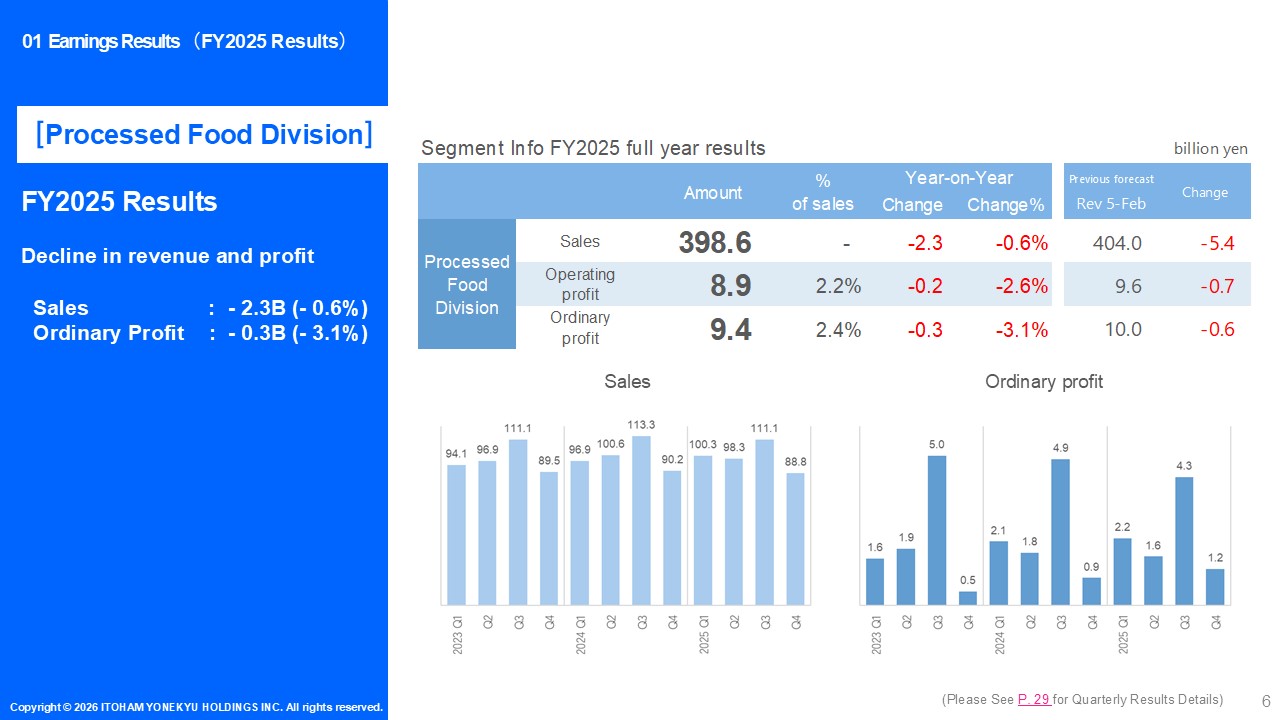

Please refer to page 6.

For fiscal year 2025, revenue in the Processed Foods Business declined by JPY 2.3 billion year on year. While we made progress in improving unit prices, we struggled to expand sales volumes, which resulted in a decrease in revenue. With respect to ordinary profit, raw material and other costs continued to rise. Although we implemented price revisions and internal improvement initiatives, ordinary profit declined by JPY 0.3 billion year on year, coming in JPY 0.6 billion below our previous forecast.

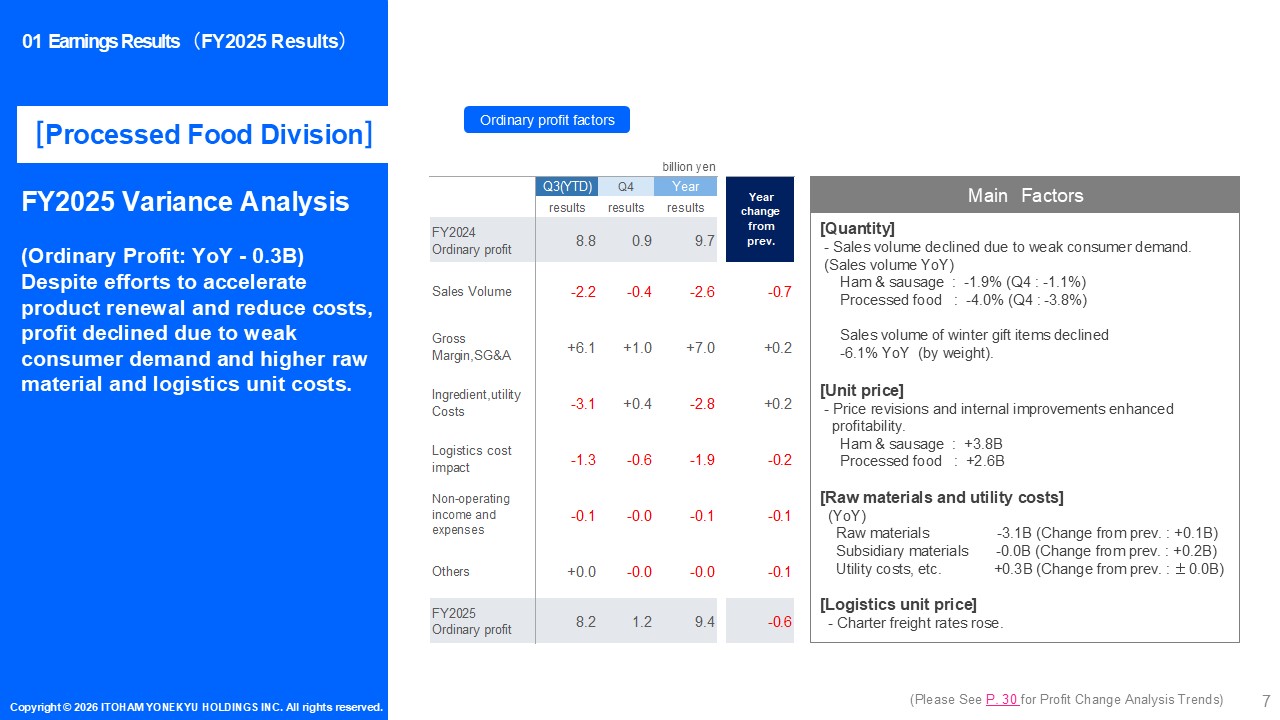

Please refer to page 7 for the profit increase/decrease analysis. First, regarding volume factors, on a weight basis, both ham and sausage products and prepared and processed foods declined year on year, resulting in a negative impact of JPY 2.6 billion. This was due to the fact that, while we proceeded with price revisions, improvements to the product portfolio, and SKU reductions, we were unable to fully offset the resulting decline in sales volumes with other products.

Next, regarding unit price factors, through the steady execution of price revisions and various internal improvement initiatives, we achieved a positive impact of JPY 7.0 billion. On the other hand, higher main raw material costs resulted in a full-year cost increase of JPY 2.8 billion. In addition, logistics cost pressures amounted to JPY 1.9 billion.

As a result, external factors had a combined negative impact of JPY 4.7 billion.

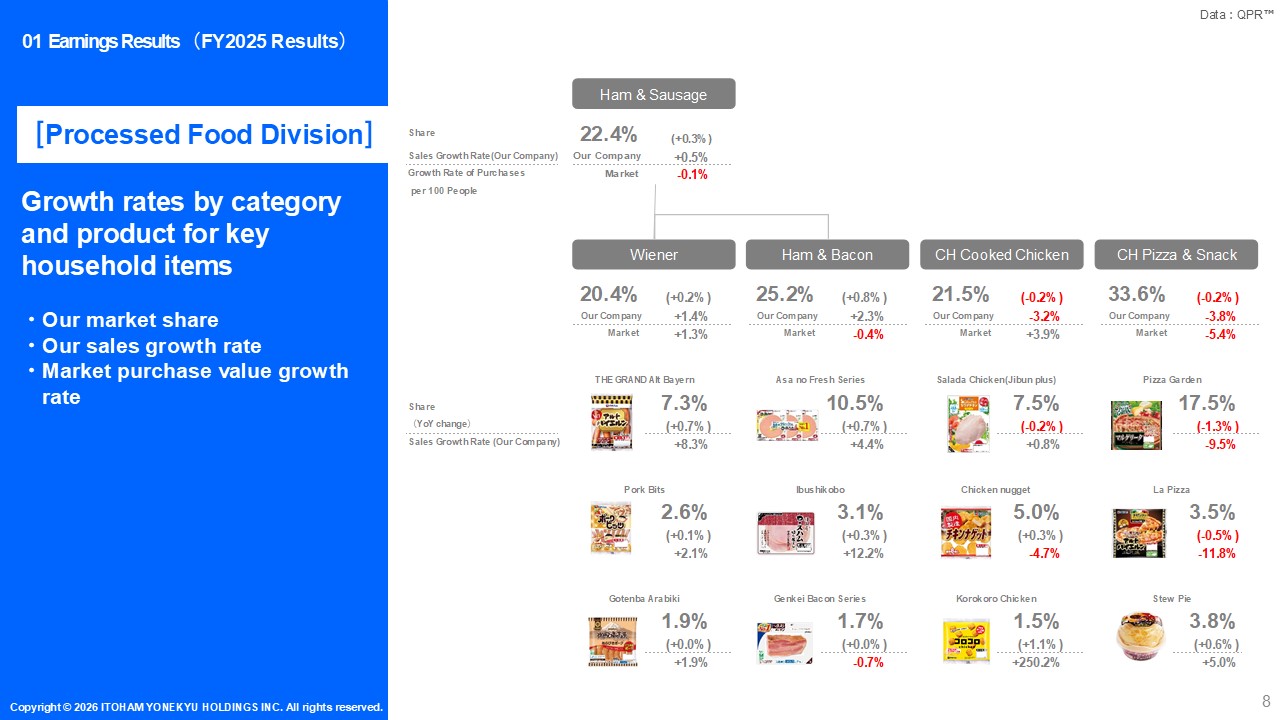

Please refer to page 8, which shows the growth rates by major at-home product categories and individual products.

Looking at growth by product, in the sausage, ham, and bacon category, we worked to strengthen and expand sales of our core brands, including Alt Bayern, Pork Bits, Gotemba Arabiki Pork, Asa No Fresh, and Ibushi Kobo. As a result, we were able to increase both revenue and market share. In contrast, Genkei Bacon saw a decline in sales volume, mainly due to the impact of price revisions.

In the chilled cooked chicken products category, competition in items such as salad chicken and nuggets has intensified. Against this backdrop, Korokoro Chicken, which was launched as a highly differentiated product, has performed well and helped support overall sales of chicken products. As for pizza, there were periods of tight production capacity in fiscal year 2024. While we implemented price revisions and aimed to achieve appropriate sales volumes, sales volumes declined more than expected.

In the current fiscal year, we will focus firmly on increasing sales volumes.

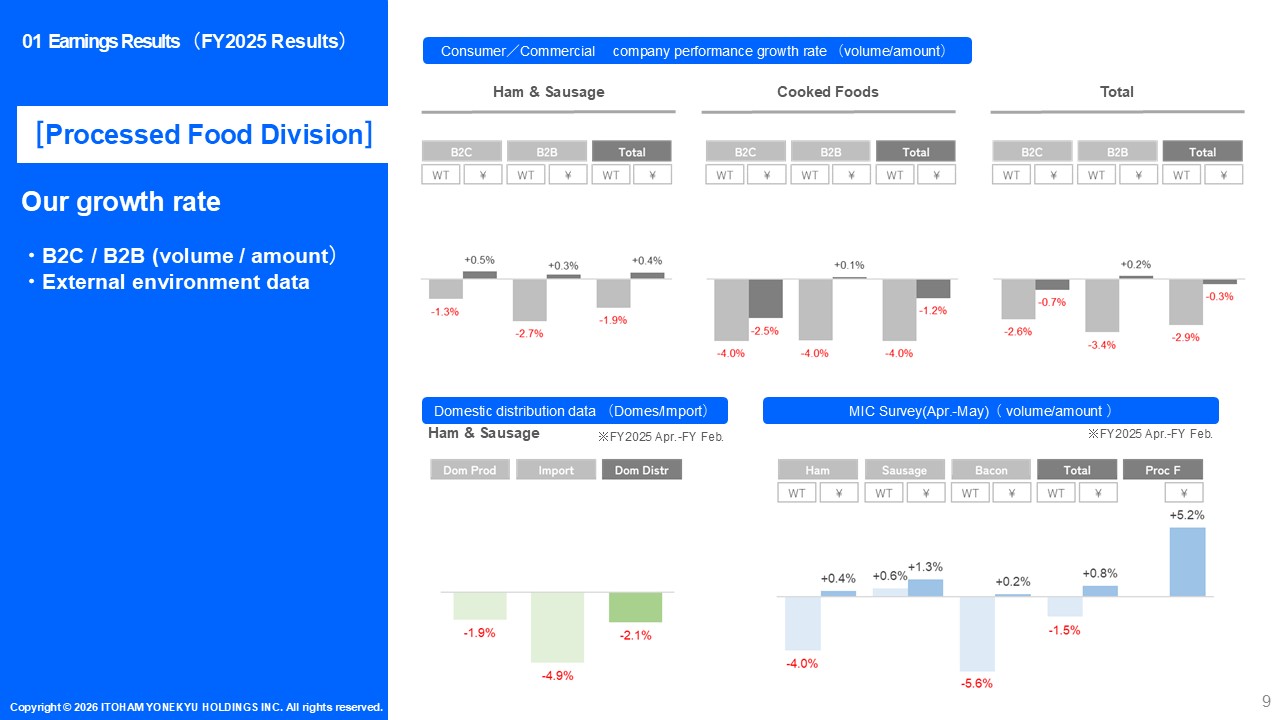

Please refer to page 9 for sales performance and growth rates.

The sales volume of ham and sausage products, on a weight basis, declined 1.9% year on year, as volumes fell in both the B2C segment and B2B channels. The overall domestic distribution volume of ham and sausage products also declined by 2.1% year on year, showing a broadly similar trend.

In the B2C segment, sales volumes increased mainly for national brands (NB); however, volumes of private brands (PB) declined, and we were unable to fully offset the decrease in PB with growth in NB. In the B2B channels, we are improving the product portfolio by implementing price revisions and withdrawing products with low volumes or low profitability.

For prepared and processed foods, sales volumes declined by 4% year on year in both the B2C segment and B2B channels, making fiscal year 2025 a challenging year. In the B2C segment, sales volumes declined for products such as pizza and hamburger steaks, while in the B2B channels, declines were seen in items such as tonkatsu. For these categories, we plan to increase sales volumes through product renewals and the introduction of new products.

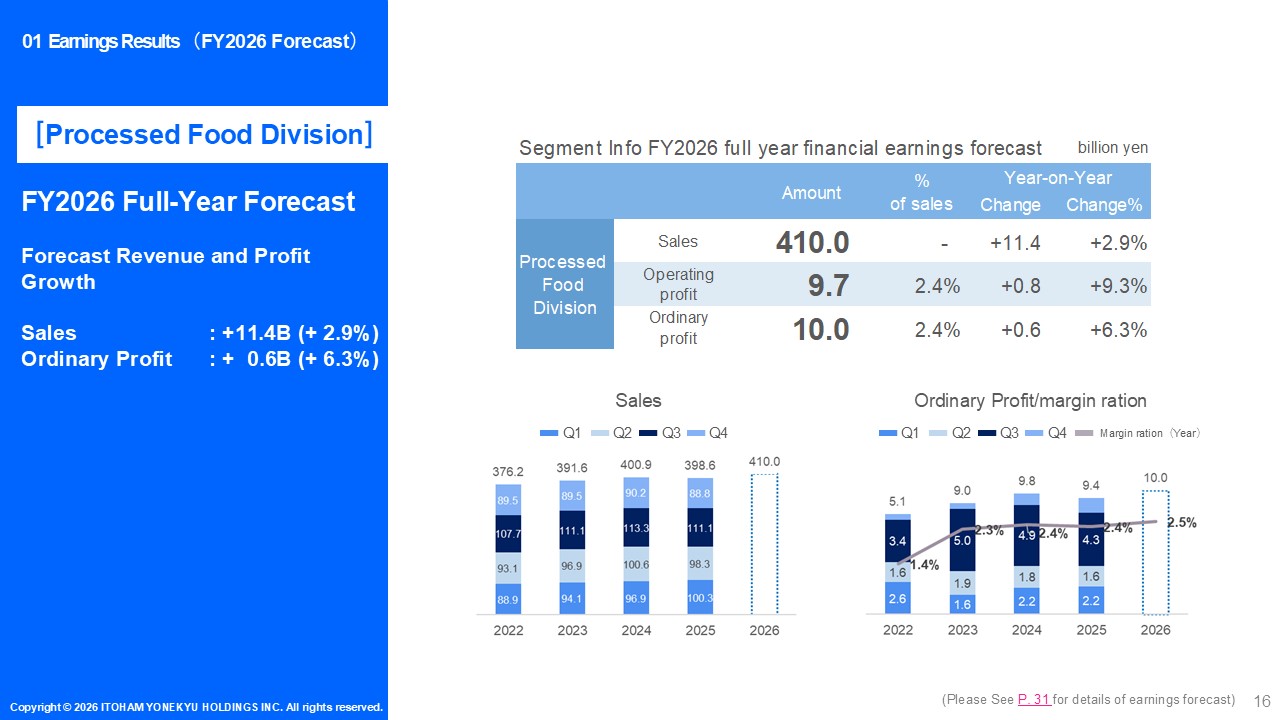

Please refer to page 16 for the full-year forecast for fiscal year 2026.

For the Processed Foods Business, we plan revenue of JPY 410.0 billion, representing a year-on-year increase of JPY 14.4 billion, and ordinary profit of JPY 10.0 billion, up JPY 0.6 billion year on year.

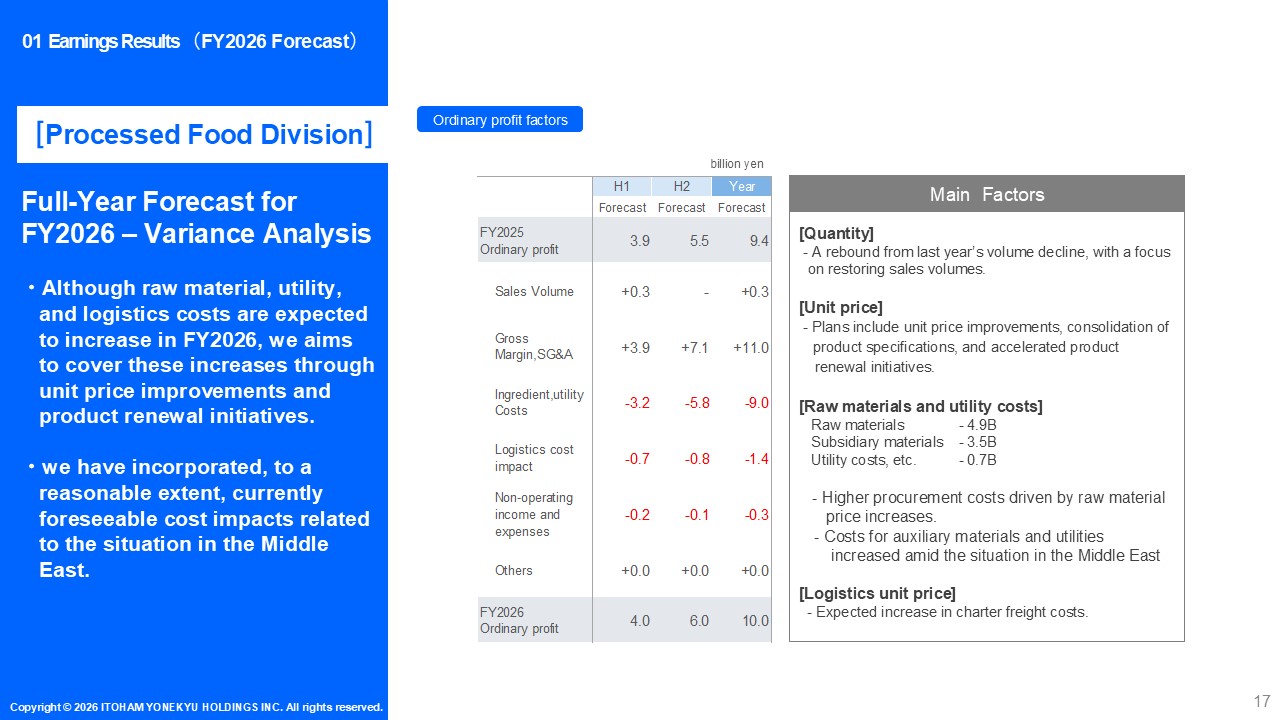

Please refer to page 17 for the profit increase/decrease plan.

Regarding external factors, we expect cost increases totaling JPY 10.4 billion. In addition to higher prices for main raw materials, particularly pork, we believe that rising costs for packaging materials, utilities, and logistics will be unavoidable due to the situation in the Middle East.

In response, we plan to continue improving internal factors, along with price revisions and accelerated product portfolio turnover, in fiscal year 2026 as well. Through these initiatives, we aim to achieve total profit improvements of JPY 11.3 billion and deliver higher profits overall.

As a result, we expect to record ordinary profit of JPY 10.0 billion for the full year.

That concludes my presentation.

Harada:

Next, Harada will explain the full-year results for fiscal year 2025 and the full-year forecast for fiscal year 2026 for the Meat Products Business.

Please refer to page 10.

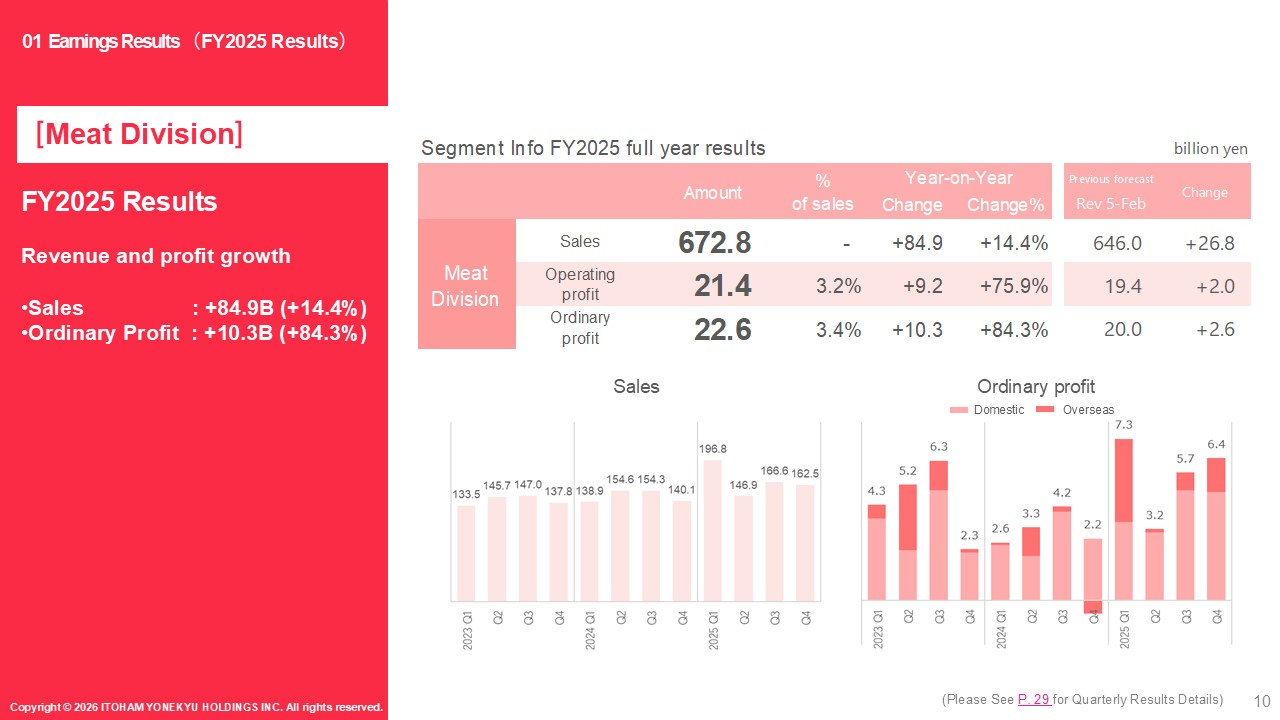

For fiscal year 2025, the Meat Products Business recorded revenue of JPY 672.8 billion, representing a year-on-year increase of JPY 84.9 billion, or +14.4%. Ordinary profit amounted to JPY 22.6 billion, an increase of JPY 10.3 billion year on year, or +84.3%.

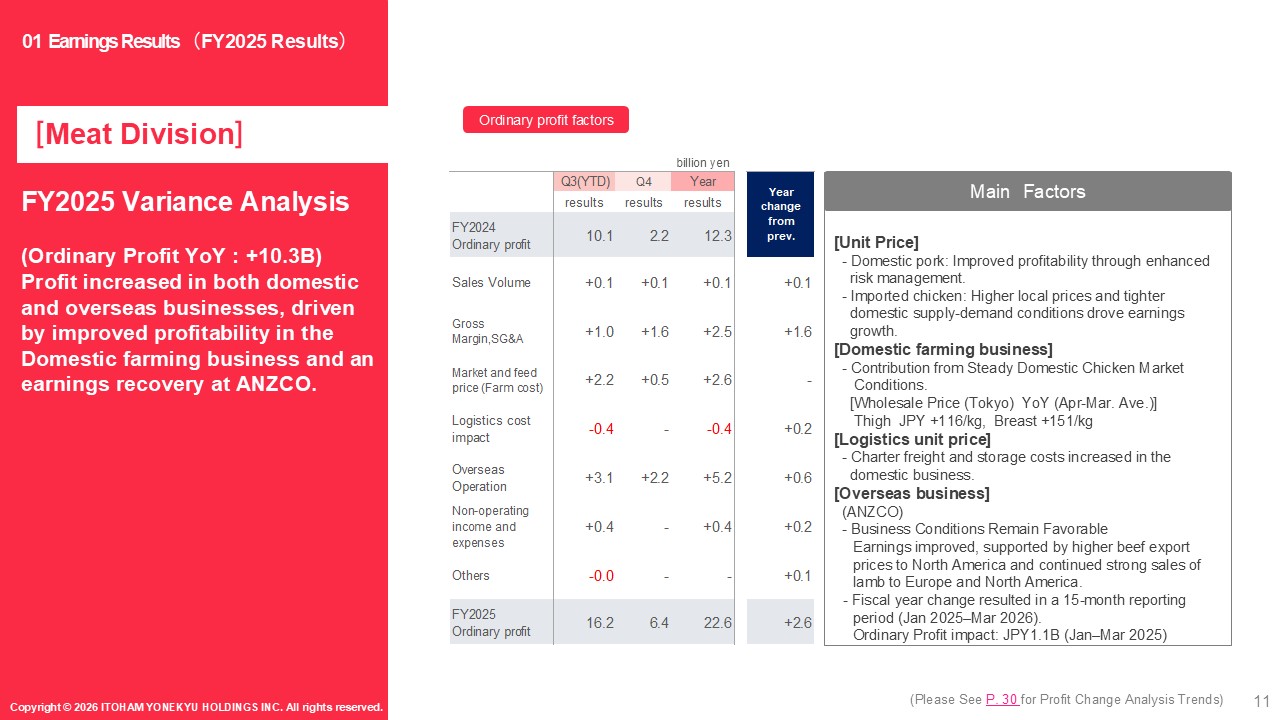

Please refer to page 11 for the analysis of changes in ordinary profit.

The increase in profit was driven mainly by improved profitability in domestic pork, favorable market conditions for imported and domestically produced chicken, and a recovery in earnings at ANZCO.

In domestic pork, we strengthened risk management by revising trading terms.

For imported and domestically produced chicken, we effectively captured the tailwind from higher market prices, resulting in increased profitability.

In the ANZCO business, earnings increased due to higher beef export prices to North America and strong sales of lamb to Europe and North America.

In addition, in fiscal year 2025, we recognized 15 months of earnings as a result of the change in ANZCO’s fiscal year-end.

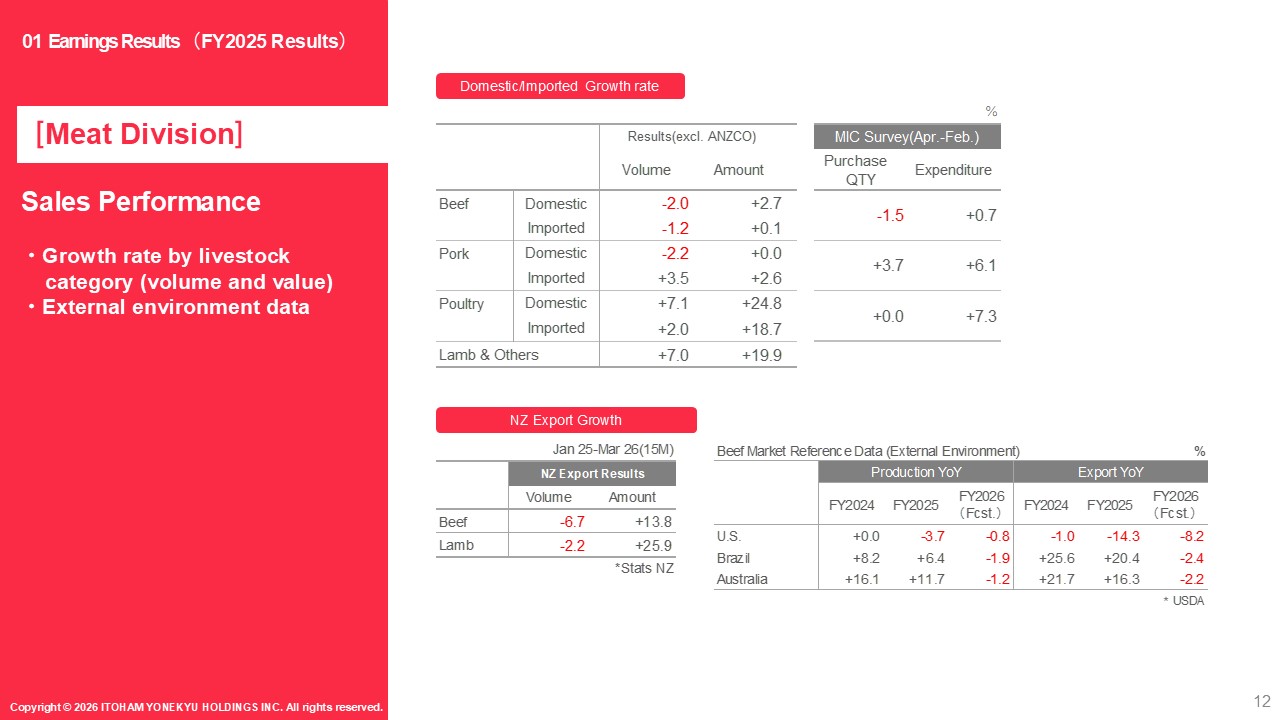

Page 12 presents the sales performance.

At the top of the page, we show growth rates by livestock category. For beef, sales volume declined year on year due to weaker consumer sentiment amid rising prices, as well as higher prices for imported beef caused by foreign exchange effects. For domestically produced pork, sales volume decreased as we intentionally reduced procurement volumes with the aim of stabilizing profitability.

Meanwhile, demand shifted toward relatively lower-priced imported pork and chicken, resulting in year-on-year increases in sales volumes for imported pork, imported chicken, and domestically produced chicken.

In terms of sales value, both domestic and imported products benefited from higher market prices, and all livestock categories recorded year-on-year increases.

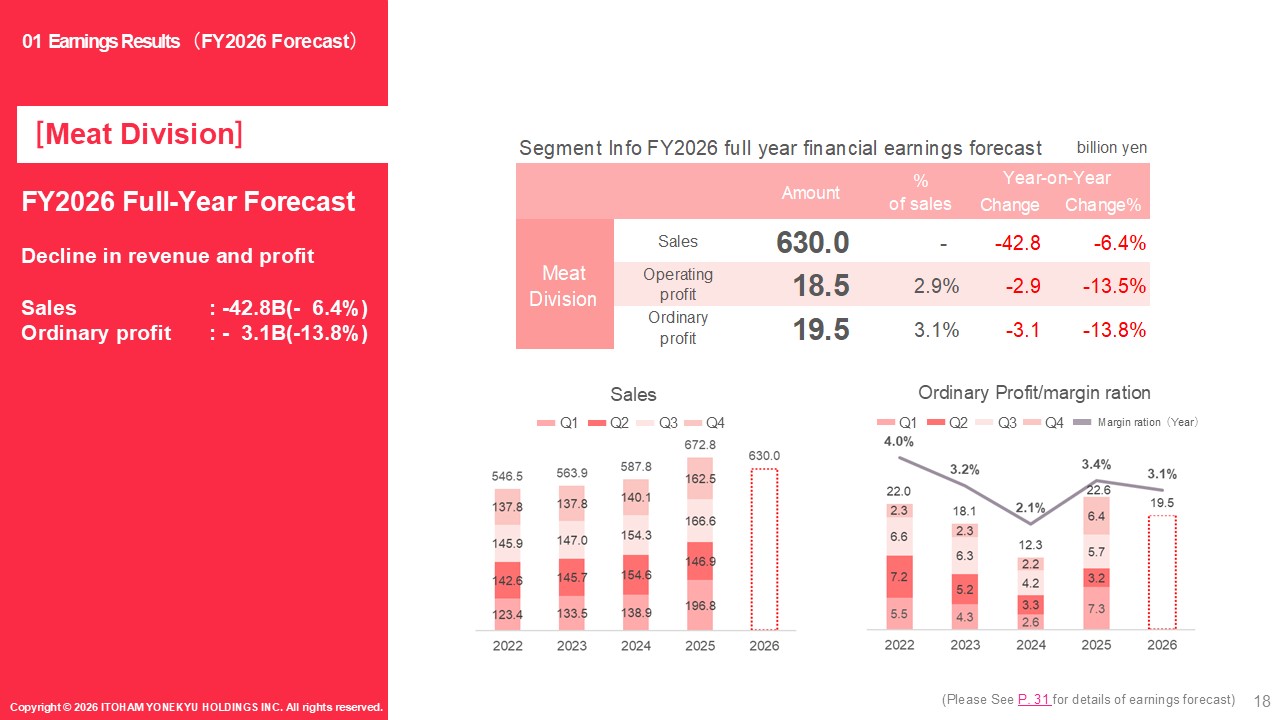

I will now explain the full-year forecast for fiscal year 2026 for the Meat Products Business.

Please refer to page 18.

For fiscal year 2026, we forecast revenue of JPY 630.0 billion, representing a year-on-year decrease of JPY 42.8 billion, or -6.4%.

We also forecast ordinary profits of JPY 19.5 billion, down JPY 3.1 billion year on year, or -13.8%.

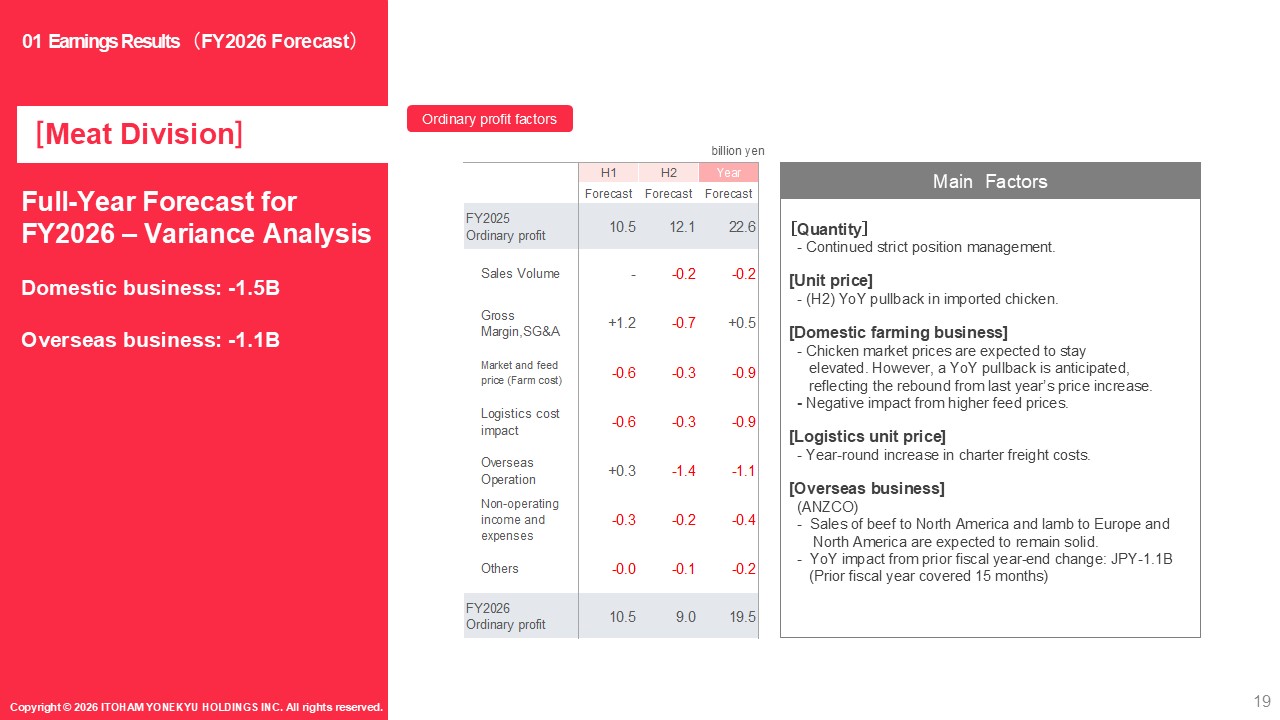

Please refer to page 19 for the factors behind the year-on-year changes in the full-year forecast.

I will focus on the key factors.

Regarding unit price factors, we assume a negative impact of JPY 0.7 billion in the second half, reflecting a reactionary decline following last year’s high market prices for imported chicken.

However, through the ongoing revision of trading terms for domestically produced pork and strict position management for imported meat, we forecast a full-year year-on-year improvement of JPY 0.5 billion. With respect to market price and feed cost factors, although chicken market prices are expected to remain elevated, we anticipate a year-on-year decrease of JPY 0.9 billion, mainly due to the reactionary decline following last year’s price increases and higher feed costs.

As for logistics costs, freight rates are expected to continue rising, and we therefore forecast a negative impact of JPY 0.9 billion year on year. Finally, regarding overseas business factors, mainly related to ANZCO, while beef transactions for North America and lamb sales to Europe and North America are expected to remain solid, we forecast a year-on-year decrease of JPY 1.1 billion due to the reaction following last year’s fiscal year-end change.

Based on these factors, we forecast ordinary profit of JPY 19.5 billion for the Meat Products Business in fiscal year 2026.

Nakao:

Next, Nakao will explain the progress of the Medium-Term Management Plan 2026.

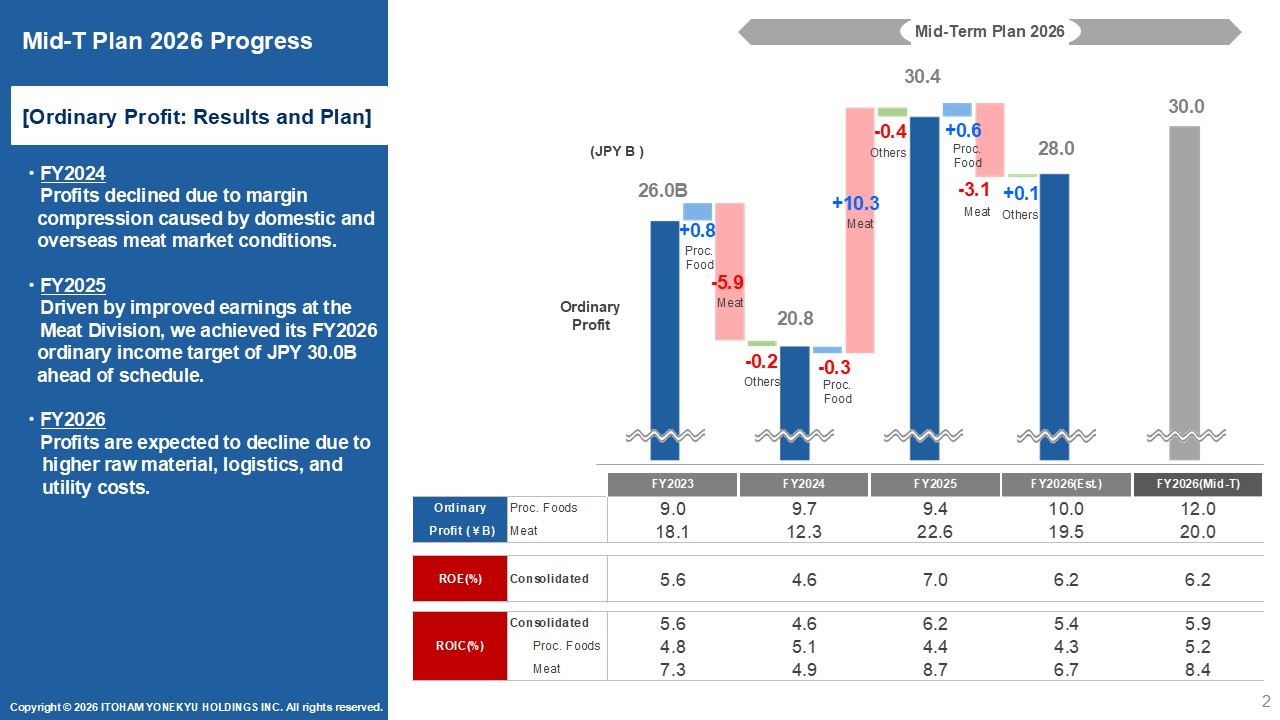

Please refer to page 2, which shows the performance trend from fiscal year 2023 through the current Medium-Term Management Plan period (FY2024–FY2026).

For fiscal year 2025, company-wide ordinary profit reached JPY 30.4 billion, achieving the Medium-Term Management Plan target of JPY 30.0 billion and marking a record high.

In fiscal year 2026, however, we expect a challenging business environment. In addition to the reversal of one-time factors seen in fiscal year 2025, rising raw material, utility, and logistics costs driven by factors such as the outbreak of ASF in Spain, a weaker yen, and the situation in the Middle East are expected to have a significant impact.

As a result, we forecast ordinary profit of JPY 28.0 billion, representing a year-on-year decline.

Accordingly, profit attributable to owners of the parent is also expected to decrease to JPY 18.5 billion, down from JPY 20.2 billion in fiscal year 2025. As a result, ROE is expected to decline to 6.2% and ROIC to 5.4%. As a company, we aim to restore ROE to the 8% range as quickly as possible.

The current Medium-Term Management Plan concludes in fiscal year 2026, and we will enter a new Medium-Term Management Plan from fiscal year 2027.

Under the new plan, we will continue to focus on strengthening our earnings base and improving capital efficiency in order to achieve an ROE of 8%.

For reference, the segment ROIC outlook for fiscal year 2026 is 4.3% for the Processed Foods Business and 6.7% for the Meat Products Business.

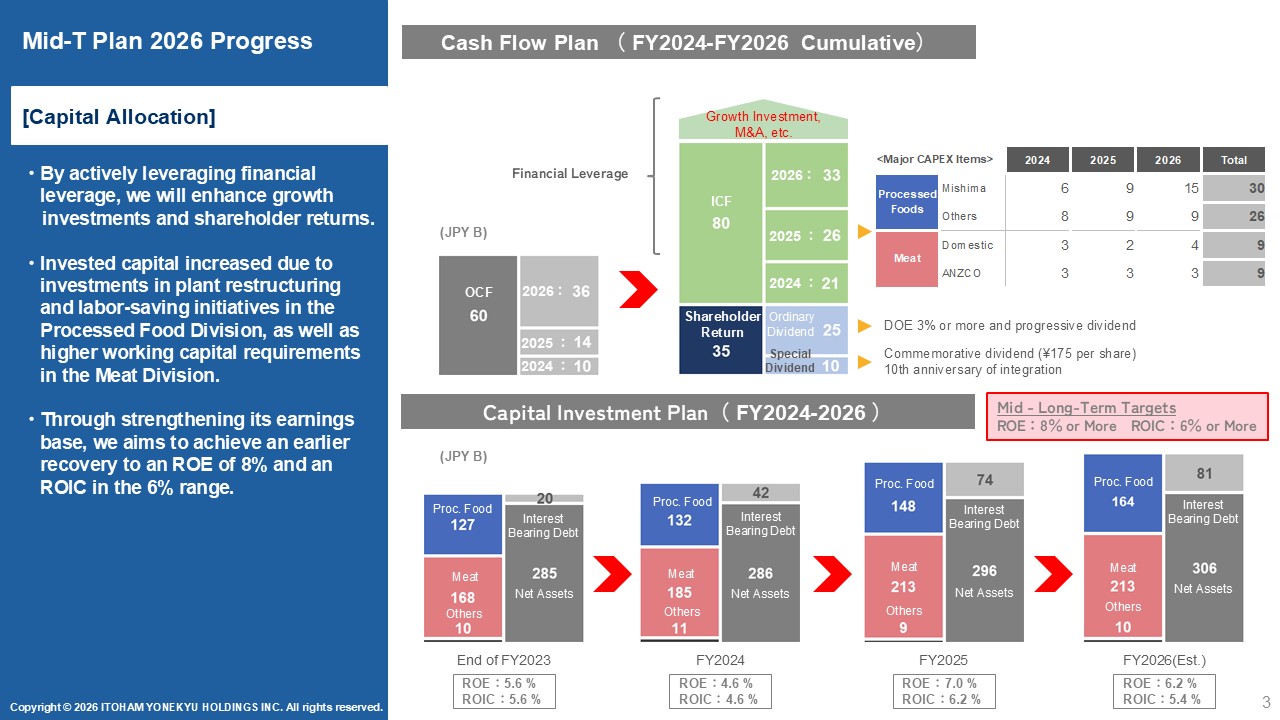

I will now explain capital allocation. Please refer to page 3.

First, we expect cumulative operating cash flow of JPY 60.0 billion over the three-year period.

Last year, we had forecast approximately JPY 80.0 billion; however, due to rising meat prices, working capital requirements increased in the Meat Products Business, resulting in a decline in operating cash flow.

As for the use of funds during the Medium-Term Management Plan period, we plan to allocate JPY 80.0 billion to investments and JPY 35.0 billion to shareholder returns, including a commemorative dividend.As a result, the combined cash flows from operating activities, investing activities, and shareholder returns are expected to result in a net funding shortfall of JPY 55.0 billion.

We plan to cover this shortfall by utilizing financial leverage. While this level is well within our financial capacity, we obtained a domestic credit rating last year in order to maintain a clear understanding of our own credit profile.

In addition, we conducted long-term funding at the end of last year, and arrangements for long-term financing toward the start of operations at the Mishima plant in fiscal year 2026 are now largely in place.

As previously explained, the dividend planned for fiscal year 2026 is JPY 155 per share, representing an increase of JPY 10 from the ordinary dividend for fiscal year 2025. This corresponds to a DOE of 3.2% and a dividend payout ratio of 48%.

Invested capital as of the end of fiscal year 2025 amounted to JPY 148.0 billion in the Processed Foods Business, JPY 213.0 billion in the Meat Products Business, and JPY 9.0 billion in other businesses, for a company-wide total of JPY 370.0 billion.

While invested capital in the Processed Foods Business was broadly in line with plan, invested capital in the Meat Products Business increased due to higher inventory-related working capital, which has been one of the factors putting downward pressure on ROIC. We will therefore renew our focus on improving working capital efficiency.

Even after taking these factors into account, we retain sufficient financial flexibility. Accordingly, in addition to improving ROE, we will continue to actively pursue investment opportunities, including M&A, to support sustainable growth.

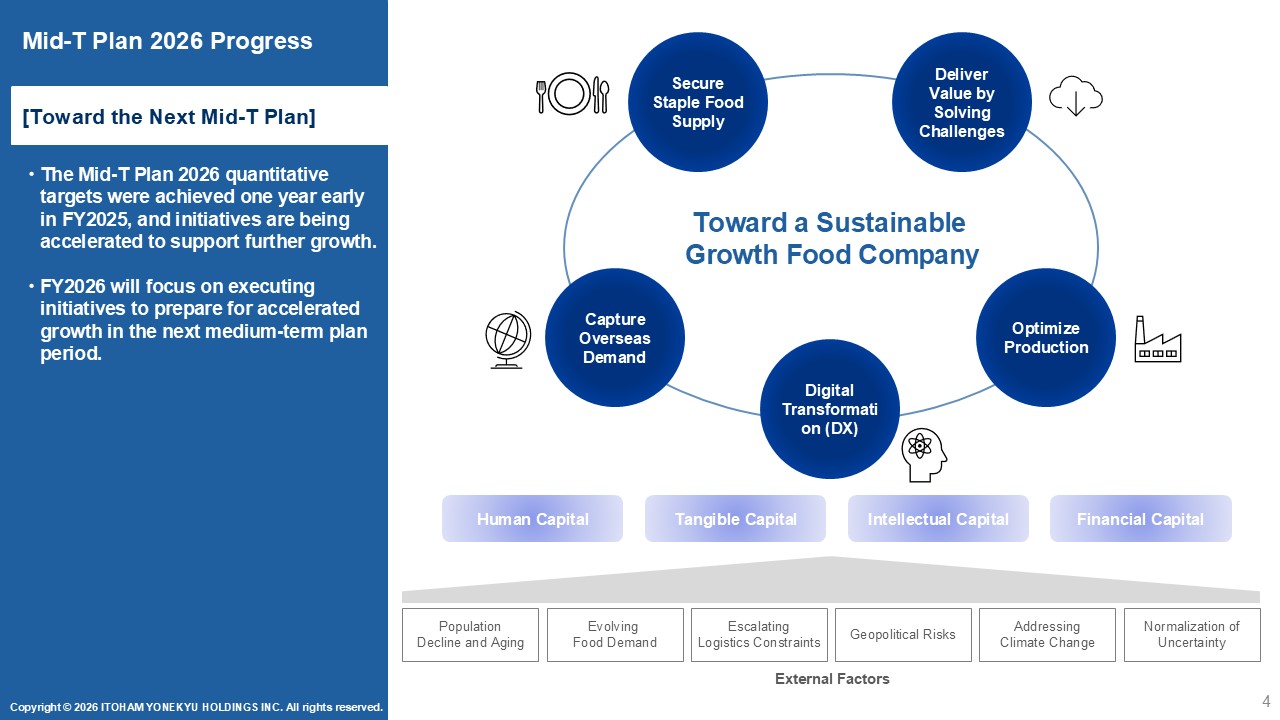

Please refer to page 4, which provides an initial look ahead to the next Medium-Term Management Plan starting in fiscal year 2027.

We recognize that the business environment surrounding the Group will remain challenging for some time, due to factors such as Japan’s declining and aging population, changes and diversification in food-related needs, the full-scale impact of logistics constraints, and geopolitical risks, all of which make steering the business increasingly complex. Against this backdrop, we aim to become a comprehensive food company that can deliver sustainable growth, and we are committed to implementing a range of initiatives to achieve this goal.

From a strategic perspective, our focus will be on enhancing our capability to supply essential food products and creating value by addressing social and customer challenges.

Specific initiatives will include capturing overseas demand, optimizing our production structure, and revamping business models that are still influenced by past commercial practices.

We also recognize the need to accelerate digitalization and update our operations for the next generation.

We will engage in intensive discussions on these topics during the current fiscal year and reflect the outcomes in the next Medium-Term Management Plan.

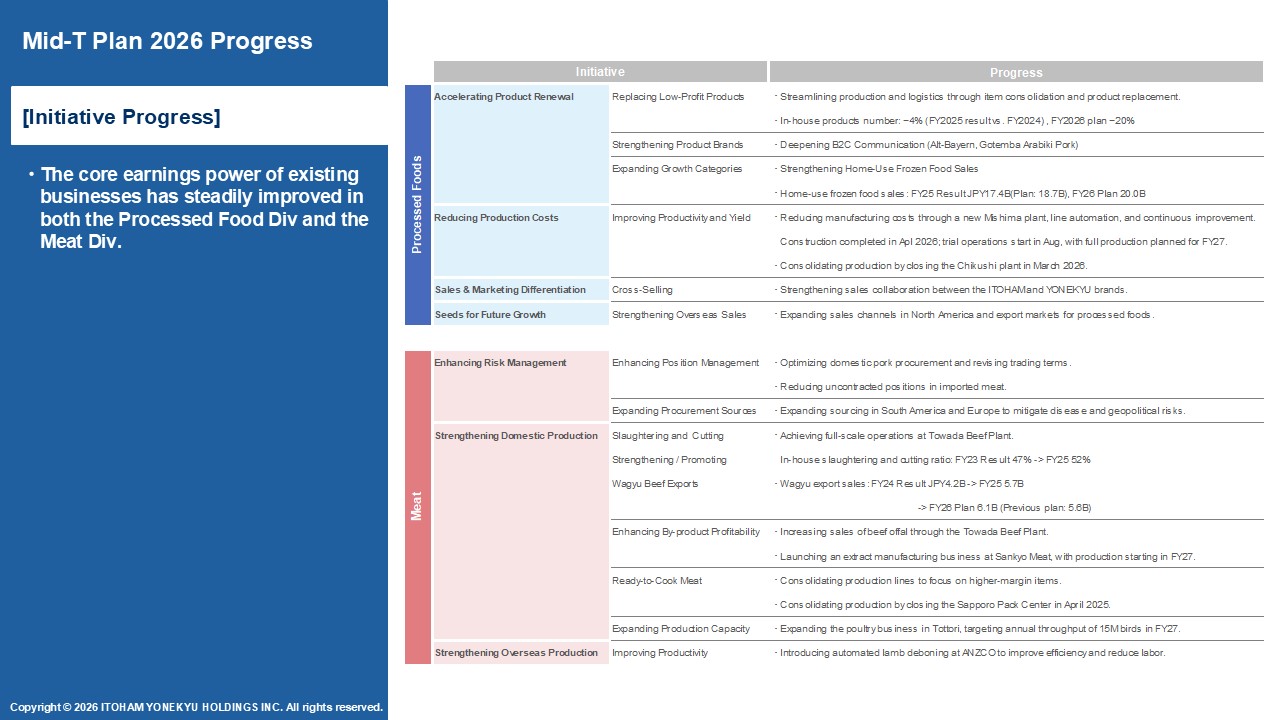

I will briefly highlight the progress of key initiatives in the Processed Foods Business and the Meat Products Business under the current Medium-Term Management Plan.

Processed Foods Business

First, regarding the replacement of low-profit products, we are promoting SKU rationalization.

We plan to reduce the number of in-house SKUs from approximately 1,300 in fiscal year 2024 to 1,100 by the end of fiscal year 2026, with the aim of improving production efficiency. As of the end of fiscal year 2025, the number of SKUs decreased by approximately 50, or 4% year on year.

While about 500 SKUs were discontinued, we also launched approximately 450 new SKUs, resulting in active product turnover.

Although the net reduction rate appears modest, we view this as evidence that product renewal is progressing steadily in line with customer demand. At the same time, given the challenging external environment, we believe it is essential to pursue production efficiency without exception.

Beyond SKU reductions, we will continue efforts such as standardizing specifications across different products to further enhance efficiency.

In addition, the Mishima plant will begin operations in the current fiscal year.

While the full benefits of this investment will be realized from fiscal year 2027, when the plant reaches full capacity, it will provide us with state-of-the-art automated production lines for sausage and raw bacon manufacturing.

Leveraging this as a foundation, we will work to optimize production structures across the Group.

Meat Products Business

In the Meat Products Business, initiatives such as revising trading terms for domestically produced pork and curbing uncontracted positions in imported meat have been highly effective and have contributed meaningfully to performance in fiscal years 2025 and 2026.

As a medium- to long-term initiative, we are also focusing on enhancing meat production capacity.

With the full-scale operation of the Towada beef plant, our in-house slaughtering and cutting ratio has increased, driving Wagyu exports beyond initial expectations.

In the chicken production business, we are expanding farming capacity, and we expect to reach annual processing capacity of 15 million birds in fiscal year 2027.

That concludes my explanation.